When it comes to automated underwriting, rules aren’t just guidelines—they are the foundation of precise, data-driven decision-making. By leveraging structured rules, insurers ensure fairness, accuracy, and efficiency in evaluating an applicant’s risk profile.

How Underwriting Rules Shape the Decision Process

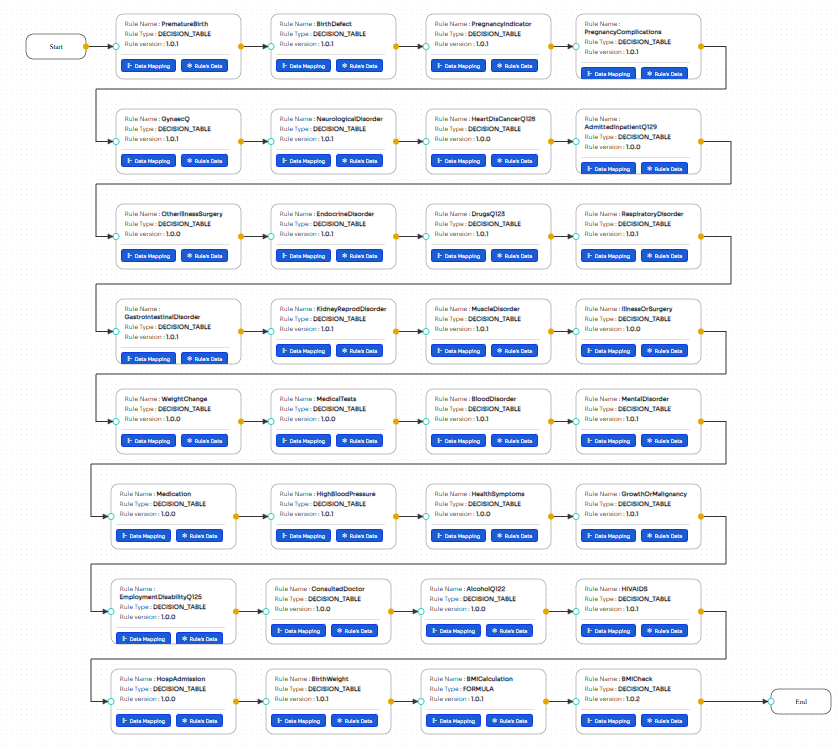

The underwriting workflow follows a systematic evaluation, starting with an initial assessment and progressing through key health factors. Each rule examines a specific risk indicator, ensuring a comprehensive, unbiased assessment before reaching a final decision.

An Example: Key Rule Categories and Their Impact

-

Pregnancy & Birth-Related Factors – Assess risks tied to premature birth, congenital defects, and pregnancy complications that may affect long-term health.

-

Respiratory & Neurological Disorders – Evaluate breathing issues and neurological conditions, ensuring these risks are accurately factored into underwriting decisions.

-

Cardiovascular & Metabolic Conditions – Identify heart disease, high blood pressure, and endocrine disorders, which are critical predictors of long-term health risks.

-

Gastrointestinal & Renal Health – Analyze digestive and kidney-related disorders, ensuring coverage decisions reflect potential health challenges.

-

Mental & Musculoskeletal Health – Incorporate conditions like arthritis and mental health disorders, recognizing their impact on both physical well-being and insurability.

-

General Health & Lifestyle Indicators – Factor in weight fluctuations, medical tests, medications, and reported symptoms to get a holistic view of an applicant’s health.

-

Serious Conditions & Risk Factors – Review past surgeries, cancer history, HIV/AIDS status, and alcohol consumption, as these directly affect longevity and risk exposure.

-

Employment & Hospitalization History – Consider whether an applicant has work-related disabilities or hospital admissions, offering insights into potential long-term risks.

-

Final Assessment – BMI & Birth Weight – The last stage involves calculating BMI, ensuring the applicant’s health indicators meet predefined underwriting standards.

Types of Rules That Power Automated Underwriting

![]() Decision Tables – Structure complex underwriting criteria into clear, rule-based decision pathways for objective risk evaluation.

Decision Tables – Structure complex underwriting criteria into clear, rule-based decision pathways for objective risk evaluation.

![]() Formulas – Used for calculations like BMI, ensuring precise assessments based on applicant data.

Formulas – Used for calculations like BMI, ensuring precise assessments based on applicant data.

The Bottom Line

Underwriting rules don’t just streamline risk assessment—they ensure consistency, transparency, and efficiency in decision-making. With AI-powered automation, insurers can accelerate approvals, reduce errors, and enhance policyholder trust.